Introduction

A commodity exchange is an organized, regulated market that facilitates the purchase and sale of contracts whose values are tied to the price of commodities[1]. On a commodity exchange, the buyers of contracts agree to accept delivery of the commodity whilst the sellers agree to deliver the commodity. The contracts traded are standardized and each specifies the quantity, quality, price and delivery mechanism of the underlying commodity. Commodities themselves are basic goods which are commercially interchangeable with others. They are used as inputs in the production of other goods and services[2]. Commodities are generally classified as metals, softs, grains and oilseeds and livestock. The metals irrespective of their characterization (base, strategic, minor and precious) are mined[3]. Almost all other commodity groupings are agricultural products – cocoa, coffee, cashew nut, oil palm, maize.

Commodities trade in two types of markets: the spot commodity market and the commodity market for forwards, futures and derivatives (options). Spot transactions take place on the spot and may take place in an auction or sales room. They are over-the-counter (OTC) transactions where the parties to the trade agree on the characteristics of the commodity. Upon agreement, the trade is executed and payment which is usually cash is made at settlement. The spot market features the immediate delivery of the traded commodity. The forward market on the other hand, is based on the delivery of the underlying commodity at a future date. Like the spot market, it is OTC traded and the contract can be tailored to the needs of the parties involved in the trade. Commodity forwards also settle cash for the underlying physical commodity.

Commodity futures differ from forwards markedly by the standardization of the exchange traded contracts. Forward markets for commodities have been around for centuries. Risk averse commodity producers and users attempt to hedge their inventories and cash flows using forward and futures contracts. These contracts offer producers stability and consistency of prices for their produce. Future contracts in particular protect farmers against drops in prices. Considering that commodity exchanges trade primarily in raw materials, producers of exchange traded commodities stand to benefit from price discovery, access to finance, hedging opportunities and market information.

History of Commodity Exchanges

Historians point to the adoption of gold coins as a medium of exchange by medieval Europe for trading with returning merchants from the East Indies and Asia as having played a critical role in the formation of formal trading markets. These developments lead to the establishment of centralized exchanges of which the 1531 stock exchange of Belgium is well documented. Commodity exchanges are believed to have emerged in the 17thcentury with the Amsterdam bourse (1695) and the Dojima rice market (1730) in Osaka are particularly mentioned. However, modern day commodity exchanges can be traced to the success of exchanges that emerged in the 19thcentury. The Chicago Board of Trade (CBOT) and the London Metal Exchange (LME) successfully launched their operations in 1864 and 1877, respectively. Multiple exchanges were created in the following years in Russia, Argentina, China, Turkey, Hungary, India and the USA. However, most of the exchanges outside the USA and Europe collapsed after the second world war due to government policy interventions. Their role and influence grew, but until the late 1980s, they remained largely confined to developed nations[4]. Market liberalization and the impetus of information technology in the early 1990s saw the proliferation of commodity exchanges worldwide. Most functional commodity exchanges are now located in Latin America and Asia[5].There has also been tremendous consolidation of exchanges in Europe and North America over the last decade. For instance, the Chicago Board of Trade and Chicago Mercantile Exchange (CME) merged in 2007 and acquired New York Mercantile Exchange the following year. Consolidation has created a smaller number of exchanges but with each exchange having more power and market share. Nonetheless, there is a remarkable growth of exchanges in emerging markets.

Ghana Commodity Exchange (GCX)

Ghana Commodity Exchange is a limited liability company which is currently owned wholly by the government of Ghana[6]. It is a membership based exchange and only members of the exchange have access to its trading platform[7]. GCX is the country’s first and only centralized market for buying and selling of physical agricultural products as well as the trading of futures and option contracts. The financial products, however, are yet to be listed and remain future milestones. The exchange is regulated by the Securities and Exchange Commission in line with the Securities Industry Act, 2016 (Act 929). The exchange commenced operations in November 2018.

Who are the Main Participants on GCX?

Commodity exchanges depend on a diverse group of participants who play distinct roles in ensuring a fully functional marketplace. Commodity producers (farmers), commodity users, brokers, traders and speculators are key actors to the operation of GCX. Producers grow (produce) the commodities that are traded on the exchange. Without the supply of the commodity to be traded, there wouldn’t be the need for an exchange in the first place. In the near future, producers should be able to sell commodities futures on GCX prior to producing the commodity. Commodity users are the individual or companies which utilize the commodities in their production processes e.g. poultry feed mills. They drive the demand for the traded commodities on the exchange. Commodity users will be able to purchase products in advance via futures contracts when these instruments become available on the exchange. Both brokers and traders act as intermediaries between the commodity producers and the users. Distinctively, brokers buy or sell commodities on behalf of their clients whereas traders trade on their own behalf. Speculators are traders who speculate (bet) on the price direction of commodities thereby contributing liquidity to the exchange.

Which Contracts Trade on GCX?

The exchange trades spot contracts. It commenced operations trading the maize spot contract. Progressively, soya bean, sesame seed and sorghum spot contracts have been listed for trading. Each traded contract is standardized and specifies the quantity, quality, price and delivery of traded commodity. The quantity is the amount of the commodity represented in the contract. It is expressed in a metric unit which in this case is metric ton. Quality specifies the features that describe the commodity being traded in the contract. For example, the contract to deliver grade 1 maize has certain physical characteristics which includes a 13% moisture content, insect damaged and immature grains within a percentage point and minimal foreign matter (0.5% max). GCX also determines the minimum price increments at which the commodity can trade. However, it does not determine the prices for the commodities. Market participants determine the prices through price discovery. The exchange also sets the delivery locations, period and mechanism for contracts. For the spots traded, delivery is at GCX certified centres within a 10-day delivery period. An extract from the maize contract traded on GCX is presented in Table 1.

Table1. Extract from GCX Maize Spot Contract

| Contract Classification | White Maize |

| Delivery Location | GCX certified warehouse |

| Trading Unit | 1 Metric Ton (1000kg) |

| Grade | 1,2,3,4 |

| Price Quotation | Prices are quoted “Ex- Warehouse”, exclusive of taxes, fees and charges |

| Trading Hours | Monday – Friday 10:00 am – 10:20am |

| Minimum Price Movement | GHS1 |

| Product Code | WM |

| Settlement Terms (Pay-in/Pay-out) | Next working day (T+1) |

| Delivery Notice | Next working day (T+1) |

| Delivery Period | T+10 (calendar days) |

| Packaging | Each grade of maize shall be packed in clean and sound 50 kg capacity polypropylene (PP) bags used no more than once prior to deposit. Delivery will be effective on Net Weight basis, which implies that weighing of maize will be done on exclusive of bags basis and no additional payment will be given for the cost of bag. |

Source: GCX Maize Spot Contract

How does GCX function?

Commodity exchanges conduct their trading business via either a pit trading system or an electronic system. In a pit trading system, traders meet face-to-face and conduct transactions through verbal interchanges at a physical location called trading pit. One party indicates an offer to buy whilst the other party expresses an offer to sell (usually on behalf of clients). If the two parties agree on a price, the trade is executed. Electronic trading has replaced pit trading in most commodity exchanges due to the advancement of technology. GCX conducts its trading business via an electronic trading platform. With the electronic platform, traders simply enter their trades (orders) onto an electronic trading platform where the system matches buyers and sellers based on a predetermined algorithm which prioritises price followed by time and client. For now, floor representatives of Exchange members must be physically present at the trading floor to key in their trades. An online system will be deployed soon which will enable trades to be executed anywhere.

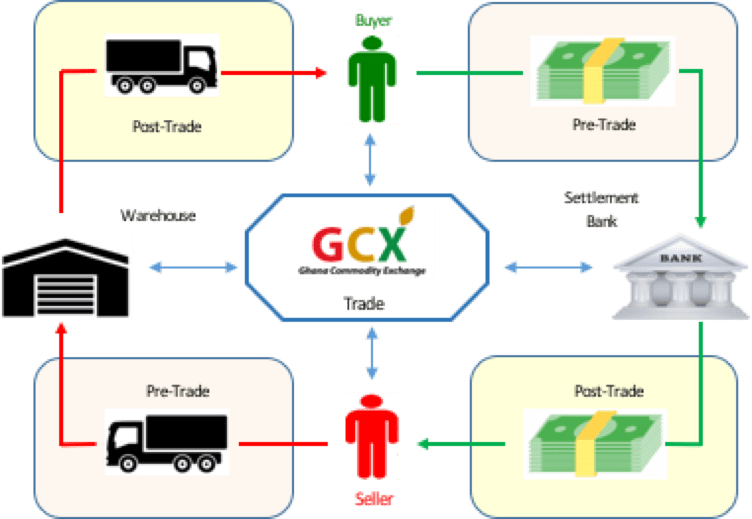

GCX also has warehouse storage operations which is linked via an electronic warehouse receipt system (e-WRS) to the trading platform. With this system, a receipt that certifies that a certain quantity and quality of a commodity has been deposited in a GCX certified warehouse is issued to the depositor (owner). The receipt (ownership title) can be transferred from one person to another. It can be used to access credit from financial institutions using the secured deposited commodity as collateral. The functional workflow of GCX from a higher level is illustrated in Figure 1. Producers of commodities who intend to sell on the exchange deposit their produce in any of the GCX certified warehouses. The warehouse receipt as aforementioned is issued to the depositor whilst the information is transmitted to the electronic trading platform. The warehouse receipt is valid for a period of 90 days during which the commodity must be traded. Buyers of commodity must have funds in their bank accounts. Member bank account balances are verified by GCX’s clearing house before a trade can be successfully executed. Once a trade deal is done, the clearing house oversees the transfer of funds from the buyer to the seller which is usually the following day. Likewise, transfer of title is issued and the buyer picks up the commodity from the delivery warehouse[8].

Figure 1.GCX Functional Workflow

Benefits of GCX

The centralisation of trade is one of the most important tools of GCX as it facilitates title transfer, price discovery, market transparency, standardization, liquidity and risk reduction. Thus, the relevance of GCX to the agricultural value chain cannot be discounted. For instance, the warehouse operations provide commodity producers, traders and commodity users reliable services such as secure storage, drying, grading and repackaging. Hitherto, producers are forced to sell their products at huge discounts since they cannot afford adequate and reliable storage facilities on their own. Moreover, the electronic warehouse receipt system helps to address the challenges faced by commodity producers in accessing capital from financial institutions. The electronic warehouse receipts can be used as secured collateral to gain capital for future productions cycles.Price discovery has long been an age-old problem in the agricultural value chain. It is known that farmers usually don’t sell their produce at the market price but do so at a price that is influenced by their desperation for cash.[9]However, through the dissemination of information generated via the trading platform, market participants become well informed and can better negotiate to boost their earning potentials. Increased flow of information through the market brings about transparency in the market and reduces short term price volatility.All commodities traded on the exchange meet the features of the standardized contract. The quality, and production period are traceable to the producer level of the specified commodity. The quality of the commodity is guaranteed by a collateral manager throughout the duration of the storage period. More so, GCX secures commodities in its warehouses and also requires buyers to deposit funds in designated settlement account prior to a trade on the electronic platform to minimise counterparty risk. Furthermore, market participants can leverage on the GCX platform to source for quality commodities at competitive prices within the West African community. Additionally, in the immediate future, GCX trading system enables all users to trade anywhere in the country, region and the world.

[1]https://commodity.com/exchanges

[2]https://www.investopedia.com/terms/c/commodity.asp

[3]Base metals (zinc, aluminum, nickel), strategic metals (bismuth, vanadium), minor metals (cobalt, chromium) and precious metals (gold, silver, palladium).

[4]Guidebook on African Commodity and Derivatives Exchanges

[5]Rashid, S., Winter-Nelson, A. And Garcia, P. November 2010. Purposes and Potential for commodity exchanges in African economies. International Food Policy Research Institute.

[6]https://gcx.com.gh/who_we_are

[7]GCX membership types include the following: Trading Members, Broker Members, Institutional Members, Associate Members and Clearing Members.

[8]All transaction (handling and trading) fees must be paid during trade settlement.

[9]Whitehead, E. 15 August 2013. Africa’s agricultural commodity exchanges take root. This is Africa of the Financial Times

Leave a comment